Startups Selling Sand in the Desert

The story of entrepreneurs who thought they were selling water in the desert and learned later that they were selling sand... like everyone else!

Today's story is about startup guys who work extra hard, match all their competitors' features, lower their prices, increase the scope of their free plan, spend millions to generate pennies, and give everything to kill their rivals because, after all, it's a war for survival! These guys are selling sand in the desert.

Most entrepreneurs compete to be the best. They think there can only be one winner, like in war or sport. To win the competition, rivals must be eradicated by relentless execution, price warfare, and constant product imitations. Those entrepreneurs live in what economists call pure and perfect competition.

The latter concept refers to a competitive state where all companies sell equivalent products, driving profits to the marginal cost of production. I confess that as a consumer, I love this zero-sum game. I remember traveling for free in 2015 in San Francisco when Uber and Lyft engaged in a price war. The same happened in Paris in 2017, where I ate at no cost for weeks when food delivery companies were involved in a race to the bottom. What else to be happy in life than free food and free transportation funded by VC money? Compete harder, please!

The ones who compete to be the best are losers. Because competition is for losers.

This form of competitive convergence is the path to mutually assured destruction. Unlike sport, there can be multiple winners in business. One should aim at being the only one selling water in the desert. The antidote to the disease of competition is a unique and singular value proposition.

Michael Porter is one of the brightest minds regarding competitive analysis. His articles What Is Strategy? (1996) and The Five Competitive Forces That Shape Strategy (2008), as well as his many books, are excellent. If you don't have time to read his complex work, I recommend reading Understanding Michael Porter by Joan Magretta.

Porter's solution to the competitive dilemma is to thrive on being unique, not the best, focusing on creating value, not beating rivals. He defines strategy as: "building defenses against the competitive forces or finding a position in the industry where the forces are weakest."

He identifies five forces that determine an industry structure, indicating its competitiveness and thus profitability.

The intensity of rivalry among existing competitors. Sometimes, rival firms are irrationally committed to the business, and financial performance isn't the primary goal. For instance, FANG companies often provide products for free, whatever the cost, to preserve their market position. What I worry the most about is dumb guys burning millions hoping to kill competitors. Look at the scooter company Bird; they raised and spent $723M for a business that is today valued at $170M. Even if you were a reasonable entrepreneur in this market, you wouldn't have survived this mindless capital allocation. (btw, thank you for the free rides!)

The bargaining power of buyers. Influential buyers can lower prices while demanding more product value. The buyer captures all value creation, not the company selling the product. Companies that sell to a highly concentrated industry, such as plane manufacturers or telecommunications carriers, deal with powerful buyers.

The bargaining power of suppliers. Powerful suppliers will charge high prices and ask for favorable terms, reducing their customers' profitability. Think about companies selling semiconductors in today's shortage. They can ask for outrageous prices because buyers have no alternatives.

The threat of substitutes. There is no high profitability if it's easy to shift to a product that offers the same value proposition. Most B2B SaaS productivity software falls into this trap. They have a lot of users but no customers paying a reasonable price because all products are the same and it's easy to switch.

The threat of new entrants. If it is easy to enter an industry by creating a similar product, then profitability will be low. Amazon Web Services enjoys significant profit because entering their industry is very hard.

I underestimated how the industry's structure determines business success. In short, as Marc Andreessen put it: the market always wins. The most determinant factor of a startup's success is the market. He wrote: "In a great market -- a market with lots of real potential customers -- the market pulls product out of the startup." "Conversely, in a terrible market, you can have the best product in the world and an absolutely killer team, and it doesn't matter -- you're going to fail."

Andy Rachleff sums it up:

When a great team meets a lousy market, market wins.

When a lousy team meets a great market, market wins.

When a great team meets a great market, something special happens.

Entrepreneurs should aim at building unique and defendable products in a highly profitable and fast-growing industry. In short, products with significant competitive moats! My idol, Warren Buffet, wrote: "We think of every business as an economic castle. And castles are subject to marauders. And in capitalism, with any castle, you have to expect that millions of people out there are thinking about ways to take your castle away. Then the question is, What kind of moat do you have around that castle that protects it?" It's not the size of the castle that matters but how defensible it is! Buffet again: "The most important thing to me is figuring out how big a moat there is around the business. What I love, of course, is a big castle and a big moat with piranhas and crocodiles."

A business protected by crocodiles, excellent! What are these moats?

Intangible Assets: benefits such as patents, brands, reputation, or proprietary process. Think about Coca-Cola, a company that has sold the same beverage since 1886 and whose brand is a childhood symbol for billions of people. Who can compete with that?

Scale: it allows a limited number of players to provide low-cost services while enjoying high margins. Think about Vanguard, which has $7.2 trillion of assets under management, allowing them to reduce commissions while still earning profits. Same for retail companies such as Cosco or insurance businesses such as GEICO.

High switching costs: it makes it costly and risky for customers to switch providers. ERP or CRM such as Salesforce or SAP are so embedded into the customer's organization that it’s impossible to drop these software.

Network Effect: when the value of a service or product becomes more compelling as more people use it. By far my favorite. Consider Facebook; it's not hard to build a similar web app, but impossible to add their 2.93 billion monthly active users who generate a great data network effect. I recommend reading the great Network Effect Bible by James Currier.

Regulation: When the laws protect incumbents with, for instance, local rules, FDA approval, or licenses. Regulation significantly increases the cost of entry and, sometimes, even avoid new entries in the market.

I like to analyze a business from the perspective of competitive moats. From my standpoint, every business attributes are either:

easy to replicate

hard to replicate

impossible to replicate

A great company has many "impossible to replicate" attributes. Teams who focus on building features similar to competitors to "match their feature sets" don't get that a great business is built on uniqueness. A good strategy requires trade-offs; it's more about what you don't do than the stuff that you do.

Go unique, or go home!

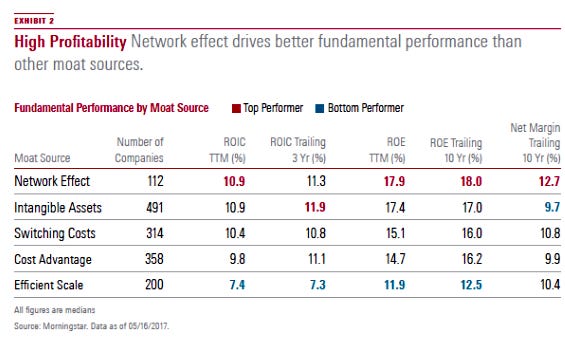

You will be pleased to know that, not all moats are created equal. Morningstar did a study comparing competitive moats and the profitability associated.

Morningstar learned that firms with wide moat are far more profitable than narrow moat firms. These wide-moat companies benefit from multiple moat sources that defend their business. Interestingly, network effect is rated the best moat, while scale is the less likely to drive great performances. What is wild is that only 10% of the 1,500 stocks that Morningstar tracks are considered wide-moat companies!

An excellent way to know if a company has powerful moats is to consider the ability to increase the price substantially. Warren Buffet said: "The single most important decision in evaluating a business is pricing power. If you've got the power to raise prices without losing business to a competitor, you've got a very good business. And if you have to have a prayer session before raising the price 10 percent, then you've got a terrible business."

My favorite burrito place in San Francisco kept raising prices, trying to keep up with inflation, so I stopped going. Restaurants are a lousy business because of the many alternatives. Sorry guys, my burrito loyalty stops at $15.

The goal of a successful enterprise is to earn profits. It means capturing the value in an industry by having a better position than rivals, suppliers, new entrants, substitutes, and even customers!

A good way to analyze a company’s performance and its competitive moats is to focus on return on invested capital (ROIC). In the long run, sustainable value creation is the difference between the return on invested capital (ROIC) and the cost of capital. What is important is the return on investment, how much capital the company can invest at a rate above the cost of capital, and for how long. The length of the competitive advantage period is crucial. According to Morningstar, the durability of economic profits is far more important than the magnitude. Quoting Buffet in his 1992 letters: "the best business to own is one that over an extended period can employ large amounts of incremental capital at very high rates of return."

Regarding capital allocation per moat-type, I like Connor Leonard's following framework:

Low/No Moat: Companies that may be perfectly well run and sell good products/services, but which do not exhibit characteristics that prevent other companies from competing away there profits if they start earning attractive returns. Most companies fall into this category.

Legacy Moat-Dividend: A company that is insulated from competition, but does not have much opportunity to grow through reinvesting cash flow. So they pay most of their cash earnings out as dividends.

Legacy Moat-Outsider: A company that is insulated from competition, but does not have much opportunity to grow through reinvesting cash flow. So they deploy their cash flow in service of acquiring other companies as well as paying dividends and opportunistically buying back stock.

Reinvestment Moat: A company that is insulated from competition and has the opportunity to reinvest their cash flow into growing the business.

Capital-Light Compounder: A company that is insulated from competition and has the opportunity to grow but which doesn't need to reinvest much cash to do so and is, therefore, able to return cash to shareholders even while growing.

The stability of the moat in time is a critical factor. Economic moats are rarely stable; they get a little bit wider or narrower every day. There is a relentless regression to the mean in which the companies' moats fade and returns trend towards the industry average.

In this matter, all industries are not created equal. Some industries have fast regression to the mean, such as the food and beverage industry, while others are slower such as the banking industry. More importantly, the long-term average mean differs between terrible sectors such as real estate or utility and good ones such as software or professional services. Anyway, there are always great defensible businesses in good as well as bad industries.

Michael J. Mauboussin did the above analysis in an article I highly recommend reading: Measuring the Moat: Assessing the Magnitude and Sustainability of Value Creation (2016). I like Mauboussin's work, which showcases a framework for analyzing different industries and companies' positions in the value chain.

Mauboussin starts by creating an industry map to understand the competitive landscape and, very importantly, the distribution of profits over time. Focusing on profits is crucial because there are businesses that build great products with millions of users but no ability to generate profits. Mauboussin then measures the industry stability, its attractiveness based on Porter's five forces, and tries to assess the likelihood of being disrupted by innovation. Pro tip: he provides a checklist of questions for assessing value creation page 53.

I think it's an analysis all companies should perform to understand their business.

Ok, ok, it is a lot. What did we learn?

Choose a highly profitable and fast-growing market

Create a product well-positioned in the value chain to capture profits

Focus on the company's uniqueness to avoid competition

Keep reinforcing the competitive moats

Reinvest cash at a high rate of return

The final competitive battle: the Startup guy vs the Intelligent CEO:

When the startup guy talks about how great the team is, the Intelligent CEO focuses on the market and industry structure.

When the startup guy talks about how disruptive the marketing is, the Intelligent CEO focuses on the position in the value chain.

When the startup guy talks about product adoption, the Intelligent CEO focuses on the durability and the widening of competitive moats.

When the startup guy talks about revenue growth, the Intelligent CEO focuses on profit and reinvesting opportunities.

Startup guys sell sand in the Sahara while Intelligent CEOs are the only ones selling water in the hot desert!

If you found this article valuable, please consider sharing it 🙌

Thanks for the great insights Nicolas. Love it.

Software is a though market, because you're not just competing with the person across the street, you're competing with the world. With just a laptop and an AWS account, anyone has access to an infinite amount of computing capabilities.

I've been thinking about startup ideas almost all my life and I don't actually think I ever came up with an idea that was truly original. You start googling and discover that lots of people have had the same idea for a long time. In order to create a monopoly, not only do you have to be right, but everyone else needs to be wrong. And that's risky business. You might end up in a blue ocean, with no competition, but also no food.

I really like the idea of choosing what not to do. It's hard, but it forces you to focus on a clearly defined value proposition. It's especially valuable for startups where you have few resources by definition and need to create some value to some customers.

Do you think "technically hard to execute" could be a defensible competitive moat ? I'm thinking of a product that's complex enough that few people would even try to copy it. You don't need to be smarter than everyone else, but you need to combine orthogonal skills that few people have. Something like, it's really hard to be the best at boxing or the best at chess, but you could become the best at chess boxing. (It's a real sport by the way: https://en.wikipedia.org/wiki/Chess_boxing)

I've got a feeling that I'm selling sand now haha! You're right in your analysis, although I would say that starting your first business as a sand seller, when you're poor, is a less risky way in life to succeed on an existing market. Especially a market where customers have already been educated by competitors, and the market research has already be done for you. That way you gain time, and the financial barrier to entry is lower in R&D. Because there's already a market and you can compete to deliver a better product at a lower price, you can still reap the benefits (although much lower in absolute value because it's obviously a race to the bottom speaking of pricing — towards being a commodity).

It's exactly what we are doing at Crisp, and to me, coming from a non-entreprenarial family, it was really the most rational bet. Crisp now provides us with plenty financial resources to settle in life, depend on no one (as self-mades), and one day become the water seller through our next venture. Only this time, taking more risks and creating an actual product which doesn't exist yet.